India’s financial system is built on several institutions that work together to maintain economic stability and provide financial assistance to individuals, businesses, and industries. Among the most important financial institutions are Banks, NBFCs (Non-Banking Financial Companies), and ARCs (Asset Reconstruction Companies).

Although these terms are often used together in discussions related to Banking & Finance Law, many people remain confused about their meaning, functions, and differences. While all three institutions deal with money and financial activities, their roles, powers, and objectives are completely different.

This article explains the meaning, functions, regulatory framework, and major differences between NBFCs, Banks, and ARCs in a simple and easy-to-understand manner.

What is a Bank?

A Bank is a financial institution authorized by law to accept deposits from the public and provide various banking and financial services. Banks form the backbone of the economy because they manage public money, facilitate transactions, and support economic growth through lending activities.

Banks operate under strict regulations issued by the Reserve Bank of India (RBI) and are governed mainly by the Banking Regulation Act, 1949.

The primary function of banks is to accept money from the public in the form of savings accounts, current accounts, and fixed deposits, and then use those funds to provide loans and credit facilities to individuals and businesses.

Banks are considered one of the most trusted financial institutions because they offer secure deposit facilities and provide customers with easy access to their money.

Main Functions of Banks

Banks perform several important functions in the economy, including:

1. Accepting Deposits – Banks accept deposits from the public through:

• Savings accounts

• Current accounts

• Fixed deposits

• Recurring deposits

2. Providing Loans – Banks provide different types of loans such as:

• Home loans

• Personal loans

• Vehicle loans

• Education loans

• Business loans

3. Payment and Settlement Services – Banks facilitate various types of Payment/Settlement services

• Online transactions

• UPI payments

• Cheque clearing

• NEFT/RTGS transfers

• Debit and credit card services

4. Foreign Exchange Services – Many banks also provide foreign exchange and international banking services.

What is an NBFC?

NBFC stands for Non-Banking Financial Company. An NBFC is a financial institution that provides financial services similar to banks but does not possess a full banking license.

NBFCs are regulated by the Reserve Bank of India under the RBI Act, 1934. Although NBFCs provide loans and financial assistance, they generally cannot accept demand deposits like savings or current account deposits from the public.

NBFCs play a major role in India’s financial system by serving customers and sectors that may not always receive adequate financial support from traditional banks. They are especially important in rural financing, vehicle financing, infrastructure funding, and small business lending.

In recent years, NBFCs have gained popularity because of quicker loan approvals, flexible documentation, and easier access to credit.

Main Functions of NBFCs

1. Providing Loans and Advances – NBFCs also provides certain loans like banks but their policies are different and they cater wider audience than banks. Some of the loans NBFC’s offers are:

• Personal loans

• Business loans

• Vehicle loans

• Gold loans

• Consumer finance

2. Asset Financing – Many NBFCs specialize in financing vehicles, machinery, and equipment. Many NBFCs play a major role in financing assets such as vehicles, machinery, and industrial equipment, especially in sectors where traditional banks may hesitate to lend quickly or flexibly. NBFCs are widely known for providing:

• Car loans

• Commercial vehicle loans

• Two-wheeler financing

• Truck and logistics financing

They often cater to:

• Small business owners

• Drivers and transport operators

• First-time borrowers with limited credit history

Unlike banks, NBFCs generally offer:

• Faster approvals

• Flexible repayment options

• Easier documentation

This makes them highly popular in India’s transport and automobile sector.

3. Investment Services – Many NBFCs also engage in investment activities, wealth management, and portfolio management as part of their broader financial services business. In terms of investment activities, NBFCs invest in financial instruments such as shares, bonds, mutual funds, government securities, and corporate debt to generate returns and diversify their sources of income. Several NBFCs also provide wealth management services, helping individuals and businesses manage their finances through investment planning, retirement planning, tax-efficient strategies, and financial advisory services. In addition, some NBFCs offer portfolio management services where financial experts professionally manage clients’ investments across multiple asset classes such as equities, debt instruments, and mutual funds with the objective of maximising returns while balancing financial risks. These services have made NBFCs an important part of India’s evolving financial ecosystem beyond traditional lending activities.

4. Leasing and Hire Purchase – Certain NBFCs also offer leasing and hire purchase facilities to both businesses and individuals, providing an alternative method of acquiring assets without making full upfront payments. Under a leasing arrangement, the NBFC purchases an asset such as machinery, vehicles, industrial equipment, or office infrastructure and allows the customer to use it for a fixed period in exchange for regular rental payments. Ownership of the asset generally remains with the NBFC during the lease term. This model is especially beneficial for businesses that want to reduce initial capital expenditure while still accessing essential equipment for operations and expansion. In a hire purchase arrangement, the customer acquires the asset by paying in instalments over a specified period while using the asset from the beginning itself. Once all instalments are paid, ownership of the asset is transferred to the customer. Hire purchase facilities are commonly used for purchasing commercial vehicles, machinery, consumer durables, and business equipment. These financing models help businesses maintain cash flow, improve operational flexibility, and expand without immediate large financial commitments, making NBFCs an important source of asset financing in India.

5. Financial Inclusion – NBFCs help provide financial services in areas where traditional banking facilities may be limited.

Restrictions on NBFCs

Despite offering a wide range of financial services, NBFCs operate with certain regulatory limitations when compared to banks. They are not permitted to issue cheques drawn on themselves and generally cannot accept demand deposits such as savings or current account deposits from the public. Additionally, NBFCs are not an integral part of the payment and settlement system in the same way as banks, which means they cannot directly facilitate payment services such as cheque clearance and interbank fund transfers. These restrictions clearly distinguish NBFCs from traditional banking institutions.

Examples of NBFCs

India is home to several prominent NBFCs that play a significant role in the country’s financial ecosystem. Some of the most well-known examples include Bajaj Finance, which is recognised for consumer and business lending; Mahindra Finance, known for rural and vehicle financing; L&T Finance, which offers retail and infrastructure financing solutions; and Tata Capital, a diversified financial services company providing loans, investment solutions, and advisory services. These institutions have become key contributors to financial inclusion by extending credit to sectors and customers often underserved by traditional banks.

What is an ARC?

ARC stands for Asset Reconstruction Company. These companies are established primarily for dealing with Non-Performing Assets (NPAs), commonly known as bad loans. When borrowers fail to repay loans for a long period, such loans become NPAs for banks and financial institutions. High NPAs negatively impact the financial health of banks. To reduce this burden, banks sell such stressed assets to ARCs. The ARC then attempts to recover the loan amount through restructuring, settlement, legal proceedings, or sale of secured assets.

ARCs are regulated by the Reserve Bank of India and operate under the SARFAESI Act, 2002.

Main Functions of ARCs

Asset Reconstruction Companies perform a specialised role in India’s financial system by dealing with stressed and non-performing assets. Their primary functions include:

1. Acquisition of Bad Loans – One of the core functions of ARCs is the acquisition of non-performing assets (NPAs) from banks and financial institutions. These bad loans are purchased at an agreed value, allowing banks to transfer stressed assets off their books and reduce financial pressure.

2. Recovery of Loans – After acquiring distressed assets, ARCs initiate recovery measures to maximise value realisation. This is typically done through:

• Negotiated settlements with borrowers

• Debt restructuring arrangements

• Legal proceedings where required

• Sale or enforcement of collateral securities

The objective is to recover as much of the outstanding amount as possible through efficient resolution mechanisms.

3. Asset Reconstruction and Business Revival – ARCs do not merely focus on recovery. In many cases, they work towards restructuring debt obligations and reviving financially stressed businesses. By redesigning repayment structures and enabling operational turnaround, ARCs attempt to restore viability to distressed enterprises.

4. Enhancing Banking Efficiency – By transferring bad loans to ARCs, banks are able to clean up their balance sheets and redirect their resources toward regular lending and core banking operations. This improves operational efficiency and strengthens overall financial discipline within the banking sector.

Importance of ARCs

ARCs play a critical role in maintaining the stability and efficiency of the financial system. Their importance lies in their ability to:

• Help banks reduce the burden of non-performing assets

• Improve liquidity across the banking system

• Strengthen financial stability

• Facilitate effective recovery and restructuring of distressed assets

By acting as a bridge between stressed borrowers and financial institutions, ARCs contribute to a healthier credit ecosystem.

India has several established Asset Reconstruction Companies that actively participate in resolving distressed assets. Some notable examples include:

• Asset Reconstruction Company (India) Limited (ARCIL)

• India Debt Resolution Company Limited (IDRCL)

• Phoenix ARC Private Limited

These institutions have played an important role in addressing bad loans and supporting the broader objective of financial sector stability.

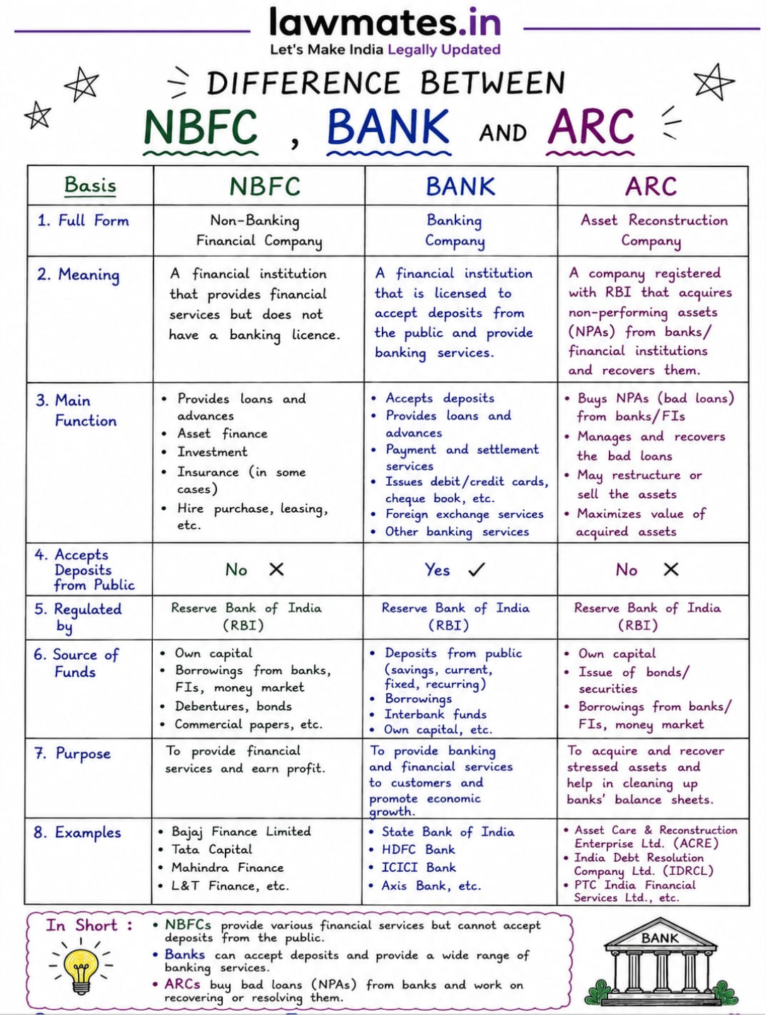

Key Differences between NBFCs, Banks, and ARCs

Although banks, NBFCs, and ARCs are all part of the financial ecosystem, they serve distinct purposes and operate under different regulatory frameworks. Banks primarily accept deposits from the public and provide a full range of financial services, including lending, payment facilities, and fund transfers. NBFCs, on the other hand, mainly focus on providing loans, asset financing, investment services, and other specialised financial solutions but generally cannot accept demand deposits or offer payment and settlement services like banks. ARCs perform a completely different role, as they deal specifically with stressed assets by acquiring non-performing loans from banks and working towards their recovery, restructuring, or resolution. While banks drive mainstream financial intermediation, NBFCs expand credit access, and ARCs help maintain the health of the financial system by addressing bad loans.

Key Thought

Banks, NBFCs, and ARCs are essential pillars of India’s financial ecosystem, but each serves a different purpose.

Banks are licensed institutions that accept public deposits and provide complete banking services. NBFCs focus mainly on lending and financial assistance without functioning as full-fledged banks. ARCs, on the other hand, specialize in acquiring and recovering bad loans from banks and financial institutions.

Understanding the distinction between these institutions is important for law students, finance professionals, businesses, and individuals dealing with the banking and financial sector. With the growing importance of financial regulation and debt recovery mechanisms in India, knowledge about NBFCs, Banks, and ARCs has become increasingly relevant in both legal and commercial fields.